The Rebalancing Bonus: Improving Investment Returns with the Kelly Criterion

Exploring whether adaptive asset allocation based on the Kelly Criterion can improve long-term portfolio returns.

This started as a rabbit hole I fell into about portfolio math and never fully climbed out of. It’s on hold now, but the calculations are on GitHub if you want to poke at them.

The Kelly Criterion is a formula from probability theory for sizing bets optimally. Applied to financial markets, even loosely, it might improve long-term returns through adaptive asset allocation. Whether it actually does is the whole question.

The Strategy

- Choose non-correlating assets

- Predict returns, correlations, and standard deviations for each asset

- Calculate the Kelly-optimal portfolio weights

- Recalculate and rebalance as market conditions change

Does it work?

Using past results to predict the future is nearly futile. But the strategy has a structural advantage: asset standard deviations and correlations exhibit momentum and can be predicted with above-random accuracy using recent historical data.

The approach: apply leverage during favorable conditions (strong negative correlations, low volatility) and reduce exposure during unfavorable conditions. Compared to a 100% equities portfolio, a Kelly-optimized multi-asset portfolio offers better downside protection at a given level of risk, which then allows leverage to be applied if the risk tolerance warrants it.

Key Assets

- Non-leveraged: VTI (US Market), VGLT (19Y Bond), GLDM (Gold)

- Leveraged: UPRO (3x S&P), TMF (3x TLT)

Predictions

Equity returns: Estimated using Damodaran’s Equity Risk Premium calculations. Research suggests equities show 10-month momentum, which may inform raising or lowering return estimates.

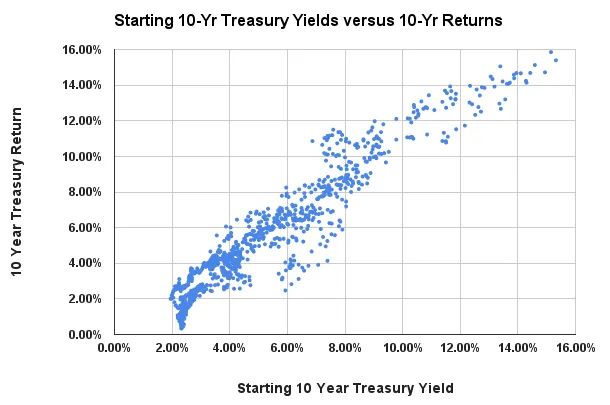

Bond returns: Equal to current treasury yield rate, with a downward adjustment when yields are below 3%.

Volatility: Averaged from 5-year historical, 20-day historical, and 30-day implied volatility.

Correlations: Averaged from 10-day, 40-day, and regime-adjusted windows.

The Rebalancing Bonus

For each asset X: SD^2 / 2 * (1 - corr) * (1 - %X)

The rebalancing bonus is relative to the Markowitz return. For a 50/50 equity/cash portfolio, the Markowitz return is the weighted average. Without rebalancing, the long-term return will deviate because of exponential growth in the equity portion. The bonus comes from systematically selling high and buying low.

The catch: if one asset dramatically outperforms another (as equities have over the past decade), rebalancing can hurt returns by trimming momentum. The strategy is most valuable when assets have similar expected returns but low correlation.

Open Research

- Predicting momentum vs. mean reversion regimes

- Optimal lookback windows for correlation and volatility estimation

- Whether Bitcoin ETFs warrant inclusion as a gold-like asset

- Smoothing implied volatility to reduce noise in allocation decisions